PUBLIC LIABILITY INSURANCE

FOR GYMS & FITNESS CLUBS

PUBLIC LIABILITY INSURANCE FOR GYMS

Fitness Industry standards packages of insurance cover appropriate for your fitness facility -

10 or 20mil Public Liability & 5mil Professional Indemnity or Civil Liability

Some gyms may also take up 1mil Management Liability.

The variables of cover limits are mainly set by the landlords who may require the highest cover even though claims history does not warrant it.

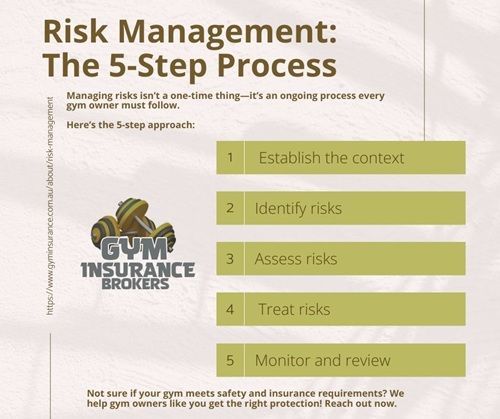

Gym owners have many tasks especially managing the risks of running their facility – from equipment breakdowns to injuries in class – but also the hassle of zeroing in on the right insurance product to cover all business operations. Due to changing policy wording and more exclusions its important to periodically check your policy with your broker. Many fitness centres are also bringing new activities like martial arts, yoga, and high-intensity interval training that may not be covered under ordinary insurance policies.

It is possible that some gyms are operating with gaps in their cover in respect to some activities not covered. Not sure about your coverage, that's why we are here as your specialist fitness and

martial arts broker.

See our gym insurance FAQ on

Home

WANT TO A

PERSONAL INJURY INSURANCE?

DO YOU LEASE A BUILDING TO RUN YOUR FITNESS FACILITY AND WANT TO COVER YOUR

CONTENTS?

Does your standard gym insurance policy cover your new kickboxing classes?

A standard insurance policy may not cover kickboxing classes even if they are just for fitness and no sparring. This a grey area of cover with the activity having to be clearly defined. Don't risk it, we have a policy that we know covers it.

How can gym owners reduce their public liability insurance?

- Have a low claims ratio and/or have high level risk management policies.

- Have the highest qualifications for their instructors and constantly improve them

- Regularly do your own or get an independent risk assessors to review/audit your facility.

- Invest in more cameras to capture incidents, making it easier for insurers to defend against a claim.

- Ask their broker for a multi policy discount (purchase a biz pack or another policy)

- Find a gym broker with preferred rates (special program) where they pass on the rates to the client.

- Be with an association with special rates, through their gym broker, that gives members discounted rates

Are you sub-leasing some gym space for martial arts (eg: BJJ, Kickboxing, MMA)?

If so you will need to make sure they have their own insurance and they are qualified to teach. There can be complications of cover if your gym members join in the martial arts classes. Ask us what you should do.

Claims can put up your insurance premium so why not jump brokers?

.Jumping brokers is not always the answer because you still have to disclose your claims history to any new insurer and they will quote based upon your historical risk. That said, your broker may suggest you ride out the increase premium for a couple of years until they drop again as you get better support if you have another claim. An experienced gym broker will know the market and unfortunately they are not a lot of players to chose from.

Why can some gym brokers get better rates for your gym and others can't?

- Brokers who belong to a buying group have greater volume and buying power to access better rates

- Some fitness brokers only have access to a couple of insurers and not from the full market

- If you have had a few claims your premium maybe loaded or declined

- You may conduct activities that only a few insurers will cover reducing your options

What is a public liability claim against a business or the owner personally?

It is a letter of demand from an individual or more than one person, for an injury sustained or personal loss at your business. This type of claim is based upon the gym owner being negligent, therefore being liable. That said, irrespective of whether the gym owner is negligent or not, this has to be proven in court. The timeline of a claim like this may take 12-18months to finalise, but some actually go run for much longer.

What should you do if you have received a letter of demand from an injured member?

A claim maybe brought against a gym several months or more after an alleged incident so the manager needs to gather information to present to their broker.

- Check to see if the member was actually at the gym at the time of the alleged incident

- Check if the incident was reported and filed

- Check if there is any video footage and witnesses

- Collect all forms of communication with the injured member

- Do not admit fault

- Do not make any payments to the injured member

- Forward all information to your broker

- Have a low claims ratio and/or have high level risk management policies.

- Have the highest qualifications for their instructors and constantly improve them

- Regularly do your own or get an independent risk assessors to review/audit your facility.

- Invest in more cameras to capture incidents, making it easier for insurers to defend against a claim.

- Ask their broker for a multi policy discount (purchase a biz pack or another policy)

- Find a broker with preferred rates (special program) where they pass on the rates to the client.

What is the obligation of the insured to minimize the chance of a claim being successful brought against them?

- make sure the insured follows their operational procedures

- provide a safe and professional environment for members to train

- make sure all instructors / coaches at the gym are full qualified for what they teach

- make sure the gym has the appropriate risk management policies in place and they are followed

- every member or person participating in any activity at your gym, needs to sign a waiver

- every person trying out for the first time needs to be fully inducted into using the equipment safely

- equipment is regularly checked for correct operation and maintained to a safe standard

- make sure the facility is clean and there are no trip or slip hazards

What are some of the fitness injuries that happen to gym members?

- tripping over a mat, weight, bag or over their own feet etc

- slipping on the soap in the shower, wet floor, wet mats from sweat

- lifting weights that are too heavy for the member

- free weights (bar bell) falling off as they didn’t clamp them securely

- free weights lying around and someone tripping over them

- falling off treadmills, bikes, steppers etc

- doing their own warm up unsupervised

- not doing an adequate warm up and working out too vigorously straight away

- not doing the exercise properly or showing off

- not listening or adhering to the instructor’s direction

- not looking where they are going and walked into walls, doors, equipment (on phone)

Ask us about our risk management strategies to help you minimize the chance of an incident.

Who are the people that claim on gym insurance?

- Those with a genuine claim due to negligence on the part of the operator and just want (reimbursement of costs)

- Those who take no responsibility for their actions and feel entitled to blame everyone else (go for max payouts)

- Those who take partial responsibility for their actions, but still feel entitled to claim (all their medical costs)

- Those who are opportunists who see an injury as an opportunity to scam the insurer (go for max payouts)

- Those who are professional scammers who fake injures and keep the claim under a certain threshold, as it’s more likely to be paid prior to going to court.

Ask us about our pre-claim strategies to help minimize the impact on your business.